Most professionals focus only on earning income.

Jun 06, 2026

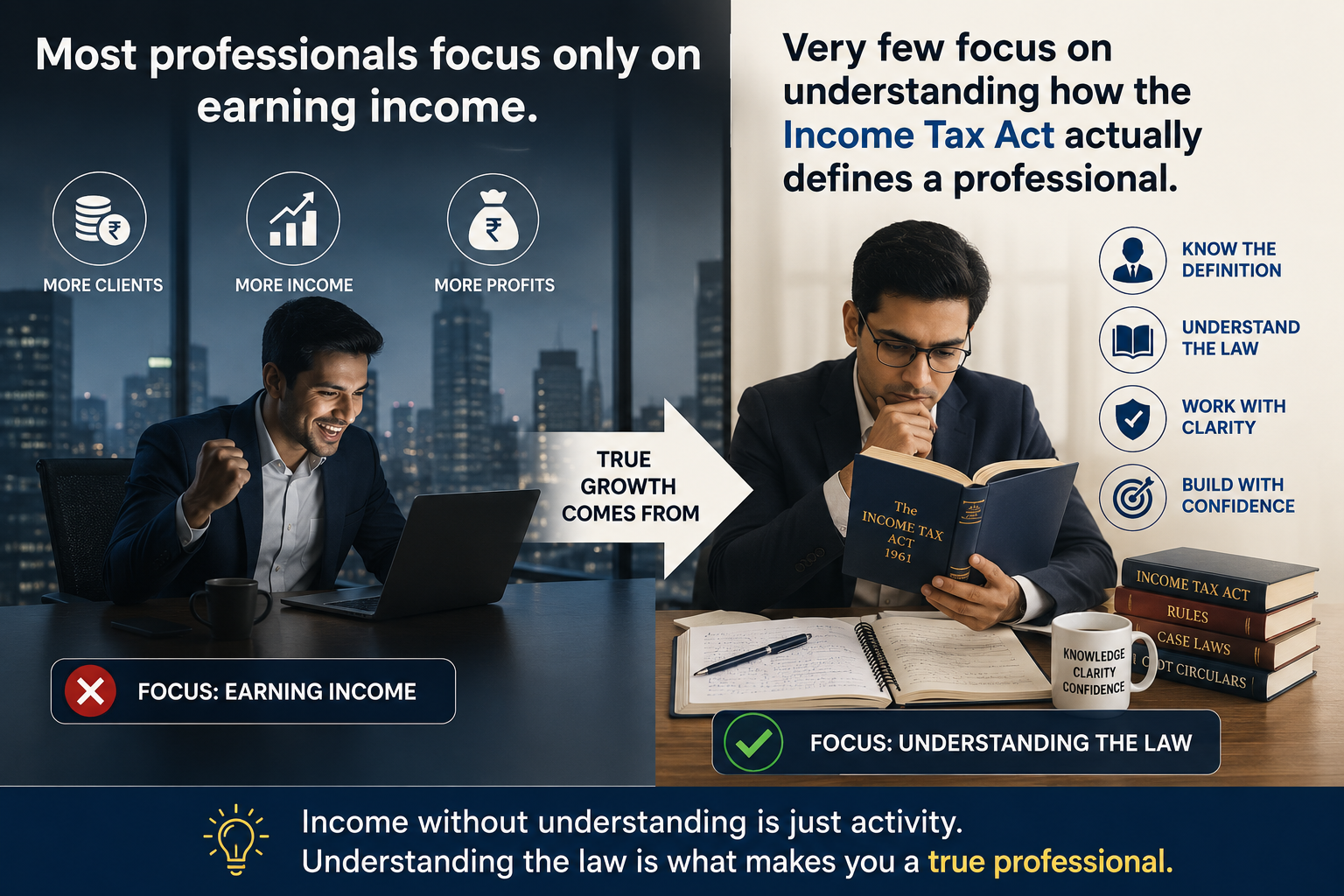

Most professionals focus only on earning income.

Very few focus on understanding how the Income Tax Act actually defines a “Professional.”

Under Section 2(36) of the Income-tax Act, the term *profession* includes “vocation” and has a very wide scope. Courts have also clarified that profession is not limited to traditional practices — it covers any specialized skill, expertise, or way of earning livelihood.

Further, Section 44AA read with Rule 6F specifically recognizes several notified professions such as:

✔ Accountancy

✔ Legal

✔ Medical

✔ Engineering

✔ Architecture

✔ Company Secretary

✔ Technical Consultancy

✔ Information Technology

✔ Interior Decoration

✔ Authorized Representatives

✔ Film Artists including actors, singers, directors, lyricists, editors, designers, writers etc.

What many people still don’t realize is that even professionals connected with sports activities like commentators, coaches, trainers, referees, physiotherapists, event managers, anchors, and sports columnists are also treated as rendering “professional services” for tax purposes under Section 194J.

Why is this important?

Because the classification of income as “Professional Income” directly impacts:

• Maintenance of books of accounts

• Tax audit applicability

• Presumptive taxation eligibility

• TDS deductions

• GST implications

• Expense claim strategy

• Compliance obligations

In today’s economy, creators, consultants, freelancers, influencers, coaches, IT experts, and service providers must understand whether their activities fall within the ambit of “profession” under tax law.

Good tax planning starts with correct classification.